What would the impact on the environment and economy be if all plastic packaging were replaced with alternative materials, like paper?

Natural capital valuation firm Trucost answers this question and more in it's new, ground-breaking report, Plastics & Sustainability.

My article on Trucost's report was published yesterday in Packaging Digest Magazine. Titled "Plastic Packaging Scores an Environmental Win," this article describes how the environment and economy would be negatively impacted if all plastic were replaced with alternative materials.

This Packaging Digest article is a revision of my original report, "Plastic: Doing More with Less, A Summary of Trucost's Plastic & Sustainability Report." Because this report was too long and too technical, Packaging Digest published a more condensed version. I have been given permission by Packaging Digest to post my original report here. I can't stress enough that though these are my words, all information is coming directly from Trucost's Report.

Click here to download "Plastic: Doing More with Less."

Learn about Dordan's sustainable thermoformed packaging.

___________________________________________________________________________________________

Plastic: Doing More with Less

A Summary of TruCost's Plastic & Sustaiability Report

Natural Capital is “the finite stock of natural assets (air, water, land) from which goods and services flow to benefit society and the economy. It is made up of ecosystems, and non-renewable deposits of fossil fuels and minerals.” [1]

Natural capital is used by the global economy to produce goods and services: Oil is extracted from the ground to power industry; trees are harvested for pulp and wood; cattle is bred and raised for human consumption. What are the social and environmental costs associated with natural capital consumption—like greenhouse gas emissions and waste management—and, who is to pay the price?

The natural capital costs of almost every product and service our economy produces and consumes is not accounted for in corporate finance, nor is it factored into the market price for a consumer product good or service. Trucost—a company working to change that—applies natural capital valuation techniques to business operations to allow corporate entities to measure environmental impacts in monetary terms. The intent is that these environmental costs can be factored into business decision-making and investment, policy setting, and in weighing the tradeoffs between implied costs and benefits of economic activity.[2]

Trucost developed a methodology for valuing the environmental cost of plastic use in the consumer goods sector for the United Nations Environment Program in 2014. Titled Valuing Plastic, Trucost identified $75 billion in annual natural capital costs associated with plastic use by the consumer goods sector.[3]

Is $75 billion in natural capital costs associated with plastic use in the consumer goods sector a lot? Trucost’s 2016 report for the American Chemistry Council, Plastics and Sustainability, works to place this valuation within a larger context by analyzing the natural capital costs associated with the consumer goods sector if plastics were replaced with alternative materials. Trucost finds—in accordance with recent studies by Franklin Associates[4] and Denstatt[5]—that a move away from plastics comes at an even higher net environmental cost, due primarily to the material efficiency of plastics vs. the alternative materials intended to replace it.

What follows is a concise discussion of Plastics and Sustainability, organized into two parts: Study Objectives & Methodology and Study Results. It is only with an understanding of the study objectives and methodology that we can arrive at an understanding of the study results; and, the implications resulting there from for enhancing the sustainability of the consumer goods sector. All information included taken directly from Plastics and Sustainability; please consult the full report for the full analysis.

Part 1: Objectives & Methodology

Trucost’s natural capital valuation framework for quantifying the environmental and social costs of plastic vs. alternative materials in the consumer goods sector works to: (1) Quantify the environmental cost of plastic used in the consumer goods sector and compare this with a hypothetical scenario in which plastic used in consumer products and packaging is replaced with a mix of alternative materials that serve the same function; (2) Map the environmental costs of plastic and alternatives across the value chain, geographic regions and consumer good sub-sectors, to target interventions to improve sustainability at these hot spots; (3) Identify those sub-sectors exposed to the greatest environmental risk if plastic were replaced with alternative materials; and (4) Quantify the potential environmental benefits of strategies to improve the sustainability of plastic use.[6]

These objectives are met via seven methodology steps—the most germane to the results included here:

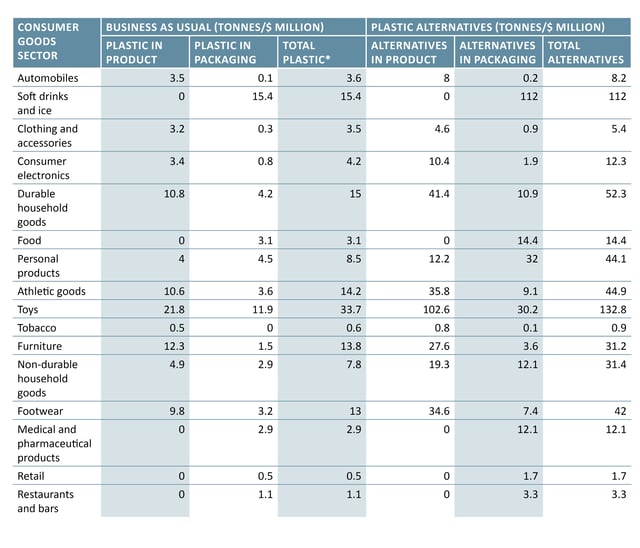

(1) Sector Selection: Trucost focused on the same 16 consumer goods sectors that were included in the Valuing Plastic report. These sectors were selected because they are significant consumers of plastic in products and packaging. These sectors are food, soft drinks and ice, tobacco, furniture, clothing and accessories, footwear, non-durable household goods, medical and pharmaceutical products, personal products, durable household goods, consumer electronics, automobiles, athletic goods, toys, retail, restaurant and bars.[7]

(2) Quantifying Plastic Demand in Each Consumer Goods Sector: Trucost estimated the total quantity of plastic demanded in each consumer goods sector using an Input-Output modeling approach to determine the expenditure of each consumer goods sector in 14 key plastic manufacturing sectors and 115 plastic commodity sub-sectors. Each of these 115 sub-sectors was used to represent a specific plastic function or application, like rigid bulk packaging or beverage containers, allowing Trucost to quantify not only the total amount of plastic used, but also the amount used for each function. This allowed Trucost to estimate plastic demand per million of consumer goods sector revenue, and when combined with estimates of sector revenue, enabled the estimation of total global plastic demand for each sector. Plastic consumption was categorized into three types: Plastic-in-product, plastic-in-packaging, and plastic-in-supply-chain, though the majority of plastic use in the consumer goods sector is used in products (31%) and packaging (46%):[8]

(3) Modeling Plastic Substitution with Alternatives: This study models a realistic scenario in which plastic used in the consumer goods sector is replaced with a mix of alternative materials that can provide the same function. Modeling a 1:1 substitution of plastics with alternatives is not realistic because plastics and alternatives have different physical and chemical properties and therefore different weights will be required of each material for a given application or function. In order to model the functionally equivalent mix of alternative materials required to replace plastic in each sector, this study builds on the work of Denkstatt (2011) and Franklin Associates (2013), which investigated the substitution of plastic with alternatives in specific product and packaging applications. Trucost integrated these findings to produce the plastic substitution model used in this study. This model includes these alternatives: Steel, iron, and tin plate, aluminum, glass, paper and paperboard, textile, wood, mineral wool, leather, residual non-substitutable plastic resin and rubber.

(4) Scope and Boundary Selection: After modeling plastic and alternative material demand in each sector, the next step was to calculate the associated environmental impacts across the lifecycle of plastic and its alternatives. The impacts included were the extraction and processing of raw materials, conversion to manufactured commodities i.e. bottles, transport to market, and the end of life fate of wastes.

(5) Impact Quantification: Trucost quantified the environmental impacts of plastic and alternative material use in the consumer goods sector using a hybrid approach drawing on Environmentally Extended Input-Output modeling and Life Cycle Analysis techniques and datasets. These approaches draw on the US Toxic Release Inventory (EPA, 2016), US Manufacturing Energy Consumption Survey (EIA, 2014), Ecoinvent Database (Weidema et al, 2013), and the US Life Cycle Inventory Database (NREL, 2013). The study includes impacts associated with greenhouse gas emissions, water abstraction, and air, water and land pollutant emissions occurring throughout the value chain. Environmental impacts occurring at end of life were quantified based on the waste management route used, including landfill, recycling, littering, and incineration with and without energy recovery. The end of life impacts of chemical additives leaching into the environment, disamenity associated with landfill and incineration sites, and the release of litter into the ocean, were also included in this analysis. An output-oriented approach was adopted to account for the avoided environmental impacts associated with the recovery of materials and energy that displace the production of virgin materials and energy from other sources[9]

(6) Valuing the Social Cost of Environmental Impacts: By comparing a business’s annual natural capital cost to its annual revenue, a company's management can understand the risk it faces if tighter regulation or consumer demand forces it to pay these costs. Trucost calculated the natural capital of material use by converting the physical quantities of different types of environmental impacts—like metric tons of particulate matter—into monetary cost and adding them together. The environmental cost intensity is the sum of all the environmental impacts expressed in monetary terms per 1M of revenue.[10]

Part II: Results

What is the global environmental cost of plastic use in the consumer goods sector and how would this change if plastic were replaced with alternatives?

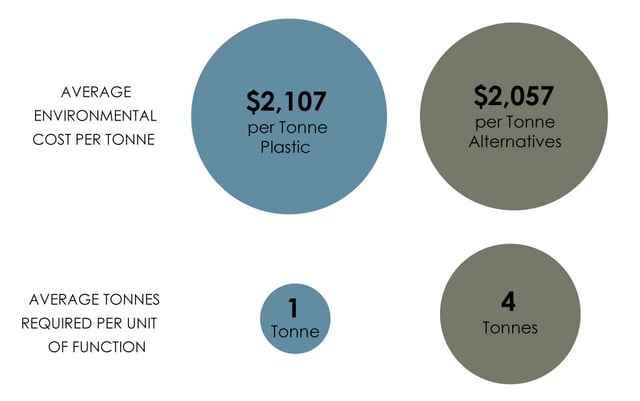

The total environmental cost of plastic use in the consumer goods sector is estimated at US $139 billion in 2015, equivalent to almost 20% of plastic manufacturing sector revenue. Trucost estimates that substituting plastic in consumer products and packaging with alternatives that perform the same function would increase the environmental cost from US $139 billion to a total of $533 billion. While the environmental cost per metric ton of plastic is greater than the mix of alternatives, four metric tons of alternative materials are required on average to achieve the same function as one metric ton of plastic. Thus plastics are more damaging to produce per metric ton, but due to their physical and chemical properties, can be used far more efficiently than alternative materials to achieve the same function.[11]

Tables provided courtesy of Trucost

What is the Impact on Oceans for Plastics and it’s Alternatives?

Trucost builds on the 2015 Jambeck et al study, estimating that over 2.5Mt of plastic marine debris was created in the consumer goods sector in 2015; this equates to between 20% and 50% of the total annual plastic inflow to the oceans estimated for all sectors in the global economy, not just consumer goods. Trucost estimates the cost of plastic marine debris created in the consumer goods sector at $4.7 billion per annum. Replacing plastic with alternatives would increase the marine debris production in the consumer goods sector by 3.4 times compared to business as usual at 8.6 Mt per annum at a cost of $7.3 billion. While the cost of ocean impacts is greater for alternatives to plastic, this is purely a function of the larger quantities of waste produced in the alternatives to plastics scenario.

The majority of ocean debris is estimated to originate in Asia, where the consumer goods sector is growing rapidly and waste management systems are under developed relative to North America and Europe. This finding is consistent with a recent study by the Ocean Conservancy (see PD article), which suggests that around 60% of plastic waste entering the ocean originates from China, Indonesia, the Philippines, Thailand, and Vietnam. Improving waste collection in these countries could have a significant impact on ocean health.[12]

Which Sectors have the Greatest Environmental Cost?

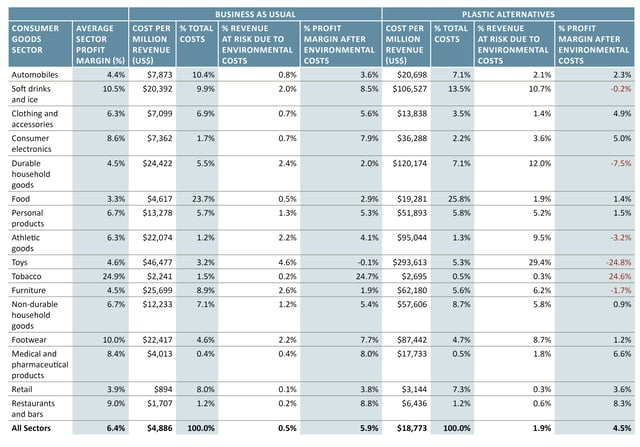

The environmental cost of plastic and alternative material use vary widely across the 16 consumer goods sectors analyzed. The environmental cost of any sector is a function of its size and relative intensity of demand for plastics, and by extension, alternative materials that serve as substitutes. The food, automobile, soft drink and ice, and furniture sectors contribute the largest share of the environmental cost of plastic use, together accounting for almost 53% of the total natural capital costs. This is due to the high plastic demand and environmental costs per million of revenue in the soft drink and ice and furniture sectors, and the higher turnover of retail and food sectors.[13]

Trucost estimates the cost of each sector if the full social costs of plastic and alternative material use were internalized as private business costs, as a proportion of the total sector revenue. The Table below illustrates the external environmental risks to sector profitability by presenting the estimated change in average profit margins for each sector if the full environmental cost of plastic or alternative material use in that sector were internalized. The revenue at risk analysis shows that for most consumer goods sectors, external environmental costs represent between zero and three percent of the total sector revenue under business as usual plastic use. Only one sector, toys, is estimated to become unprofitable under a full environmental cost internalization scenario, with revenue and all other costs held constant. Switching to plastic alternative materials would increase the proportion of revenue at risk on average across all sectors by a factor of four. Profitability is at greatest risk in the soft drink and ice, durable household goods, personal products, athletic goods, toys, furniture, non-durable household goods, and footwear sectors, with post internalization profit margins becoming negative in the alternatives to plastic scenario, with revenue and all other business held constant. Consumer goods sector profitability is at greatest risk in heavily plastic dependent segments with narrow profit margins.[14]

Table provided courtest of Trucost

Due to the different types of plastics used, and the different functions they perform, in different consumer goods sectors, the relative advantages of plastic over alternatives can vary widely. While environmental costs are estimated to increase across all sectors with the replacement of plastics with alternatives, the magnitude of this change ranges from a factor of 2 to 3 in the furniture, automobiles, and clothing and accessory sectors, to a factor of more than 4.5 in the soft drinks and ice, consumer electronics, household durables and non-durables, and toys sectors. The toys sector is the most plastic intensive sector modeled and the environmental costs associated with this sector would increase by a factor of 6.3 if plastics were replaced with alternatives.

The change in environmental costs is greatest for packaging applications, increasing by a factor of 4.2 across all sectors when plastics are replaced, compared to 3.4 for plastic use in products. This highlights the greater material efficiency of plastic in a broad range of packaging applications compared with alternatives—with less material needed to achieve the same outcome. [15]

What are the Most Important Environmental Costs and where are they Concentrated in the Value Chain?

The environmental cost of plastic use in the consumer goods sector are dominated by greenhouse gas emissions (51%) and land and water pollutants (22%), with small contributions from air pollutants (12%), external waste management costs (11%) and damage to the oceans (3%). Land and water pollutants emissions dominate the environmental costs of alternatives at 40% of total costs, followed by greenhouse gas emissions (34%), air pollution (13%), and waste management costs (11%). Greenhouse gas emissions from consumer goods sector plastic use are estimated at over 565 Mt of C02 equivalent, or 6.7 metric tons C02e per metric ton of plastic used. This compares favorably with alternatives to plastic in aggregate at 1,446 Mt C02e. However, the higher greenhouse gas emissions from alternatives are purely a function of the increased quantities of alternative materials required.

The greatest share of environmental costs are created upstream via material production and transport to market, in both the plastics and alternatives to plastics scenarios. Approximately 82% of natural capital costs associated with plastic use in the consumer goods sector occur upstream, while in the alternatives to plastic scenario a slightly greater proportion (87%) occur upstream. The operations and supply chain of the plastic manufacturing sector account for approximately 43% of the environmental costs associated with plastics use, highlighting that sustainable strategies implemented by the sector could have a significant impact on total environmental costs. Avoided environmental costs due to the recovery of materials through recycling or energy recovery through incineration, are small relative to the overall costs of material use in both scenarios. This suggests that while recycling and energy recovery can contribute to reducing environmental costs, in the case of consumer goods sector plastic and alternatives use, the greatest environmental return on investment is likely to arise from more efficient product and packaging design, and processing technologies that use less material per unit of function.[16]

In conclusion, Trucost’s natural capital valuation of plastics vs. its alternatives in the consumer goods sector demonstrates that substituting plastics with other materials that perform the same function comes at a net environmental cost of about 4 to 1. While plastics consume a lot of natural capital during production and transport to market vs. it's alternatives, the inherent material efficiency of plastic allows it to perform the same function with less mass. Trucost provides insight into the environmental hot spots of plastic use in the consumer goods sector, demonstrating that the largest return on investment for natural capital consumption occurs upstream during resin processing and transport

[1] Rick Lord & Libby Bernick. 2016. Plastics and Sustainability: A Valuation of Environmental Benefits, Costs and Opportunities for Continuous Improvement. [Online]. Available: https://plastics.americanchemistry.com/Plastics-and-Sustainability.pdf.

[2] Lord & Bernick, Plastics and Sustainability. Executive Summary. P. 3.

[3] UNEP. 2014. Valuing Plastics: The Business Case for Measuring Managing and Disclosing Plastic Use in the Consumer Goods Industry. [Online]. http://www.unep.org/gpa/Documents/Publications/ValuingPlasticExecutiveSummaryEn.pdf.

[4] Franklin Associates. 2013. Impacts of Plastics Packaging on Life Cycle Energy Consumption and Greenhouse Gas Emissions in the United States and Canada. [Online]. Available: https://plastics.americanchemistry.com/Education-Resources/Publications/Impacts-of-plastic-packaging.pdf.

[5] Denkstatt. 2011. The Impact of Plastics on Life Cycle Energy Consumption and Greenhouse Gas Emissions in Europe. [Online]. Available: http://denkstatt-group.com/files/the_impact_of_plastic_packaging_on_life_cycle_energy_consumption_and_greenhouse_gas_emissions_in_europe.pdf.

[6] Plastics and Sustainability. Executive Summary. P. 2.

[7] P. 16.

[8] P. 16.

[9] P. 19.

[10] P. 20.

[11] P. 23.

[12] P. 27.

[13] P. 28.

[14] P. 28-30.

[15] P. 32.

[16] P. 34.